Picking up where we left off with the first piece in this series (here), we were exploring the potential upside of AI-driven personalization and found there is little in the way of current case studies or research, beyond some statistics first cited in 2015/16, that attempts to quantify the impact of personalization. So the next step is to dig deeper into what the experts are saying more recently to see if we can find clarity. This is a complex topic so…

As mentioned previously, Boston Consulting Group (BCG) has an entire practice centered around personalization (https://www.bcg.com/capabilities/marketing-sales/personalized-customer-strategy-in-the-age-of-ai) that offers a number of relevant articles. Mark Abraham and David Edelman from BCG even published a book about it in 2024, (https://www.amazon.com/Personalized-Customer-Strategy-Age-AI/dp/1647826276) with the central idea being that

“A personalized customer strategy, and the ongoing cycle of activities that power it, creates a competitive moat…”

This was the most comprehensive recent attempt to quantify the impact of personalization that I could find, and it is worth taking a critical look at what they had to say and the metrics they provide.

In the book’s Preface, one of the authors shares how a solar panel company won his business by tailoring its pitch— they “…orchestrated a personalized value proposition for what is fundamentally a commodity item, albeit one whose implementation is complex.” Their edge? Optimizing the sales process ahead of competitors. The purchase was high-cost, high-involvement, and one-time, meaning personalized data was always going to be part of the equation. The company simply used it earlier in the process to boost conversions—clever, but not a lasting advantage. Plus, the data wasn’t truly "personalized" to his behaviors and preferences—just smart use of publicly available home-related info. Not to mention he had already decided to buy the product, so his critical decision was only about selecting the vendor.

Other examples provided include Netflix, which benefits from personalization through higher retention and long-term customer value, and a wine retailer that similarly utilizes rich data on behaviors and preferences to fuel personalized messaging and drive increased spend.

A general concern about the way the authors presented their anecdotes is that they imply a one-size-fits-all approach is appropriate; it is hard to make that leap because these observations would not necessarily translate to the purchases in other categories. Compare those cases above, for example, with a retailer like Starbucks, which has similarly rich data but less upside for personalization since coffee buying is so habitual, and most consumers are not looking for variety or exploration. Or a CPG/grocery purchase, which has lower spend levels and little opportunity for expanded consumption.

The introductory examples set the stage and the first chapter then lays out the thesis:

Personalization = f [ scale (volume of data) * v2 (speed of learning) ]

This is not a formula to assess impact, simply a philosophical statement about the “how” of personalization, that it is a function of availability of data and speed of response. Subsequent parts of the book suggest an implementation model and deployment considerations. This discussion will focus on the first chapter only, as that part of the book is the most relevant here.

- “Personalization is a $2 trillion opportunity”

- “Our research shows the payoff: an almost $2 trillion prize in accelerated growth awaits personalization leaders this decade.”

- “Over the next five years, the net effect will be an almost $2 trillion shift in revenue share, as personalization leaders capture the bulk of growth in their respective sectors, at laggards’ expense.”

Those statements are confusing – is personalization a $2 trillion growth opportunity, or will leaders in personalization capture $2 trillion in revenue shifted away from laggards? Or are those similar numbers merely coincidental, and both are true? Not clear what they mean, but the different interpretations suggest very different opportunities. (Put in context, if 2023 GDP is $27.4 trillion and consumer spending represents nearly 68%, that means that over 5 years, personalization would still account for less than 2% of GDP. Is that significant enough to merit all the current buzz?)

The chart shown below doesn’t help – the headline talks about a revenue shift, but the chart header and accompanying note talk about growth. (As a sense check: NRF forecast retail sales growth of $0.05 trillion from 2023 to 2024, only 1/12th of BCG’s projected $.6 trillion over five years, so there is ground to make up. And you would have to attribute 100% of industry growth to personalization, which is a stretch.) So the methodology, especially with n = 87 observations spread across seven categories, would make me very cautious about projecting these results across verticals and across the entire consumer economy and setting unrealistic expectations.

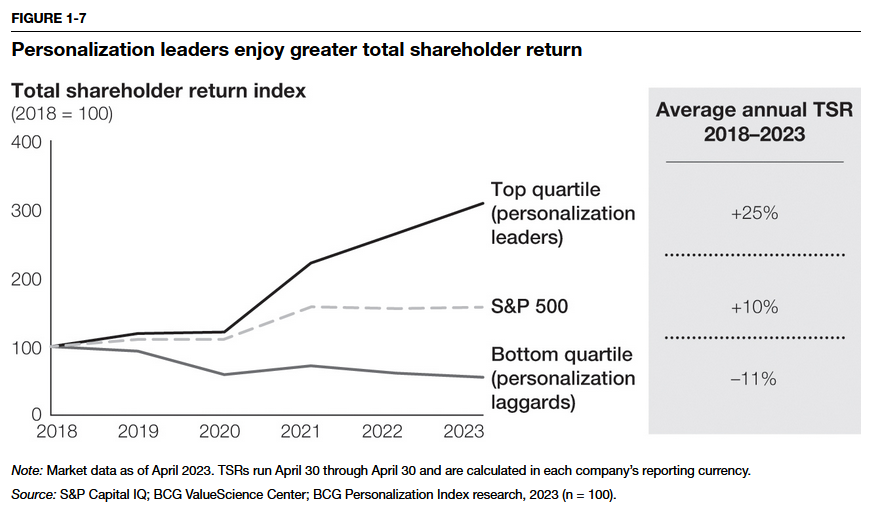

o “Personalization leaders enjoy greater total shareholder return.”

Personalization leaders (top quartile) achieved shareholder return 25% above S&P 500 average. But correlation is not causality – could it be that category leaders were already performing better, have deeper pockets and are just early adopters in personalization?

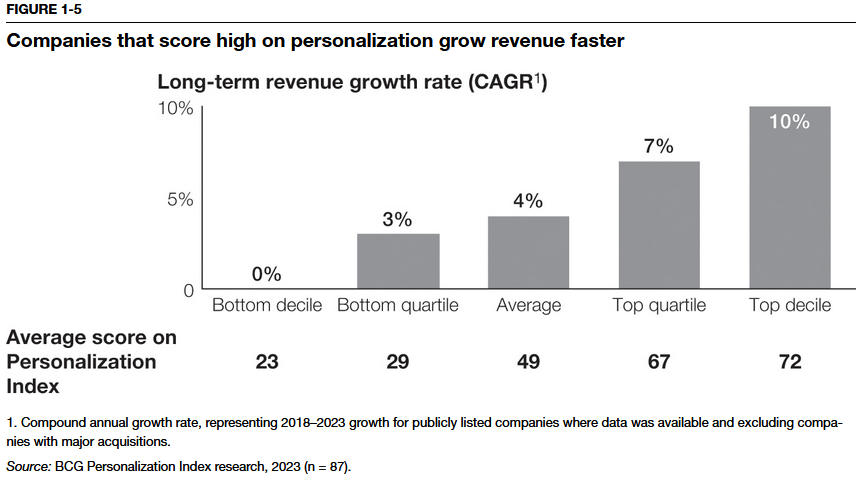

o “Leaders in personalization grow revenue ten percentage points faster annually than laggards and enjoy higher customer satisfaction scores”.

This methodology is not forward looking, meaning they looked at where companies score in terms of personalization in 2023, and then assessed how they performed over the previous five years, when personalization may not have been deployed. Better approaches might be assessing how companies scored on personalization at a previous point in time and then reviewing how they performed financially in subsequent periods, or assessing current score and reviewing down the road, but either is hard to do. For example, how do you assess slow- or no-growth impact? And there is the same concern with sample size raised earlier. So again, hard to draw a causal line between personalization and financial performance with this approach, and caution is warranted in projecting the 10% higher growth.

An adaptation of the book appeared in HBR in late 2024 and included one additional metric (https://hbr.org/2024/11/personalization-done-right ) that was attention-getting:

o “The data shows that personalization leaders have more digital customer relationships, and their customers spend 30% more than customers as a whole in their category (emphasis added). The root cause of this difference is that their customers engage three times as often (not just by transacting but also pre- and post-purchase) as do the customers of their competitors. As a result, the leading companies generate more data and insights on which to base future personalized interactions.”

What are they really saying here, that personalization leaders should be outpacing their competitors in terms of growth and share by a wide margin? That seems to be the interpretation. But the small sample size just prevents one from accepting this blanket statement without an extreme degree of caution, and there is still an issue with causality.

Overall, the book is an interesting read and takes a provocative position, but I can’t help think there’s something missing in this analysis, something still unexplained about how exactly (and how much) personalization drives long-term competitive advantage. It’s a leap to go from anecdotal stories and analysis of a small sample to the types of hard metrics declared in the BCG book and the McKinsey articles, that are still being quoted ten years on. It certainly doesn’t seem like there are insurmountable barriers preventing all players from adopting personalization – in many cases, it is only foresight and willingness to deploy resources that allow development of a scalable personalization solution. And after all, companies have been collecting and analyzing data for years, deploying segmentation and earlier attempts at personalization long before the advent of “AI-driven personalization”, and few have been able to use that to build a “competitive moat” that drives growth year-after-year.

There are many factors impacting performance. It is hard to imagine success or failure depending so heavily on where businesses stand in terms of personalization. So back to the original question: what is the potential upside? We'll attempt to come up with an approach in Part 3.

View original on LinkedInWant to discuss this further?

Our team thinks about these problems every day. Let's start a conversation.

Book a discovery call